Apollonian

Guest Columnist

FTX ON STEROIDS: IS “TETHER” THE BIDEN WORLD’S CRYPTO BCCI?

Published: November 20, 2022SOURCE: 2ND SMARTEST GUY IN THE WORLD

Link: https://www.blacklistednews.com/article/83795/ftx-on-steroids-is-tether-the-biden-worlds-crypto.html[numerous vids at site link, above]

A simple crypto rule to live by: any token or exchange that has a CEO, identifiable individual or development team associated with it is not real crypto; it's the antithesis of crypto.

This substack has been warning for quite some time that all of these centralized exchanges are nothing more than grifting operations, IRS reporting nodes and CIA black ops money laundering facilitators.

I have been warning since around 2019 that Tether is the single most egregious crypto scam out there. It is far worse than FTX, with Sam Bankman-Fried (SBF) and his team of scammers having had direct ties with Tether. The sordid cadre of snake oil salesmen behind Tether makes SBF look like an ethical player.

Tether is made possible by the CIA, and in particular the Democratic party of the illegitimate Federal government that has been laundering money to Ukraine using both FTX and Tether.

This substack has covered the criminal CIA and taxation:

2nd Smartest Guy in the World - Original Social Engineering Sin

“...the socio-psychological foundations of socialism is identical to that of the foundations of a state, if there were no institution enforcing socialistic ideas of property, there would be no room for a state, as a state is nothing else than an institution built on taxation and unsolicited, noncontractual interference with the use that private people c…

Both the CIA and taxation happen to have literally funded the likes of FTX and Tether while protecting these criminal exchanges and centralized “backed” tokens from the very investigations that the unconstitutional three letter agencies are allegedly tasked with enforcing.

2nd Smartest Guy in the World- -FTX was a Democrat Money Laundering Operation with Wall Street Dark Money & PSYOP-19 "Pandemic" Ties

The story of the scam that was FTX is going to be epic when discovery takes place for all of the upcoming trials. In the meantime, here are some of the latest facts about this crypto Ponzi exchange: There is a lot more to this story, and it intersects with all of the usual Cult players, from BlackRock to the CIA to the WEF and various “nonprofit” slush fu…

The FTX collapse has incontrovertibly proven that all of my warnings and misgivings were correct.

It is now only a matter of time before Tether is blown up too, and that may be one of the causes and/or excuses for the global financial crash to end all crashes that will most conveniently be leveraged into ushering in the Great Reset.

Since FTX was laundering for the WEF, and FTX was directly involved with Tether, it then follows that the WEF was always tethered to Tether.

All of these centralized exchanges and tokens are just the latest One World Government money laundering setup.

And the payoff will be even more ingenious: the elimination of all centralized exchanges and tokens due to a sudden global “regulation” epiphany.

Of course, said “regulation” epiphany will then be aggressively enforced only after the max amount of money laundering and wealth extraction from all of the debt-slave tax donkey crypto

And when the likes of the WEF, CIA, Democrat party and One World Government have determined that their centralized crypto scams are no longer effective, they will unleash regulations, 51% BTC attacks and wipe out the current crypto ecosystem exactly in the same manner that they will wipe out the wholly untenable global financial markets. This twin financial demolition will further strip the freedoms of humanity and usher in a global CBDC that will be inextricably tethered to the social credit score system, replete with CO2 monitoring and never-ending “vaccine” compliance.

Below is a must read expose on Tether and its ties to FTX, the CIA, and the One World Government:

by revolver

Just days ago, Bloomberg estimated 30-year-old Sam Bankman-Fried’s (SBF) personal wealth at an astonishing $16 billion. Now, the disgraced FTX founder is essentially bankrupt, and if there is a shred of justice in the world, soon headed for prison.

The collapse of FTX and its founder is one of the most spectacular implosions in history. There is no shortage of narratives to mine for interesting article fodder. Celebrities like Tom Brady and his now ex-wife Gisele lost millions to the scam. Silicon Valley “smart money” that was hopelessly entranced by a wunderkind founder. SBF also used his filthy stolen lucre to become one of the largest donors in left-wing politics of the past four years. There’s also the FTX pet philosophy of “effective altruism,” the cult-like fad ideology of contemporary Silicon Valley that SBF exploited to conduct his fraud and justify taking enormous risks. There’s also the 28-year-old girlboss CEO of Alameda Research Caroline Ellison, who bragged that her vast financial empire only requires “elementary school math” to turn profits, and whose public list of turn-ons includes “controlling major world governments.”

Oh, and there’s also the group sex (don’t worry, everyone involved in this “polycule” situation is hideous).

All of these storylines are being regurgitated ad nauseum by countless other media outlets. The story that Revolver is about to tell you is even bigger and more spectacular than all the other fascinating storylines listed above. In fact, dear reader, FTX may not even be the biggest scam in crypto. Another, even more spectacular scam may still be live, ready to collapse at any moment… if anyone decides to take a real look at it.

The story you’re about to hear concerns the third-largest crypto-currency on the planet, which you’ve probably never heard of. It is a story of how a former Disney child-actor — a Jeffrey Epstein associate who was embroiled in an under-age sex scandal — bizarrely emerged as one of the world’s strangest crypto-currency moguls. It is the story that raises serious questions as to whether an entire cryptocurrency is a scam — effectively a private money-printer. And to top it all off, there is reason to believe that if this cryptocurrency is the scam that it appears to be, it will nonetheless be allowed to continue because of this particular cryptocurrency’s usefulness to intelligence agencies in funneling money to foreign rebel groups and jihadis with plausible deniability.

Sound crazy? Sound interesting? Strap in, it’s about to get wild.

USDT, or Tether, is what is known as a “stablecoin.” A stablecoin is a cryptocurrency that, instead of fluctuating in value, is intended to hold to a consistent price. Tether is a USD stablecoin — each Tether is supposed to be equal in value to one U.S. dollar. While most cryptocurrencies are wildly speculative and backed by essentially nothing, each Tether is supposed to be backed directly by a U.S. dollar, or an extremely liquid, reliable investment like a U.S. treasury bond.

These USD stablecoins are used on cryptocurrency exchanges to conduct on-the-blockchain trades in lieu of using actual U.S. dollars. Without stablecoins like Tether, the current crypto ecosystem simply would not exist. There are multiple USD stablecoins, but Tether is by far the most popular. According to coinmarketcap.com, Tether has the third highest market cap of any crypto currency at $66 billion, trailing only Bitcoin and Ethereum. Today, fully half of all bitcoin trades globally are executed using Tether.

A year ago, crypto news site Protos summarized Tether this way:

Did that last sentence set off any alarm bells? It should have. Alameda Research is the quantitative trading firm founded by Sam Bankman-Fried. Bankman-Fried and his partner in crime, Alameda CEO Caroline Ellison, allegedly propped up their trading firm by plundering FTX customer accounts.If cryptocurrency was an engine, Tether (USDT) is one of its pistons.

Over the past seven years, the maverick stablecoin has evolved into a primary crutch for the ecosystem. It’s a tool for onboarding new money, managing and growing liquidity, pricing digital assets, and generally oiling crypto markets to keep them smooth.

Tether boasted a $1 billion market capitalization when Bitcoin hit $20,000 at the end of 2017. This year, it’s a $70 billion-plus powerhouse.

Practically every crypto exchange supports USDT trade in some form. The makeup of Tether’s reserves and its inner workings are yet to be disclosed in clear detail.

Still, the question of who exactly buys Tether directly from its parent company Bitfinex has remained unanswered since its inception way back in 2014.

Earlier this year, Protos shed light on that mystery by reporting that just two companies, Alameda Research and Cumberland Global, were responsible for seeping roughly two-thirds of all Tether into the crypto ecosystem.

[Protos]

The inner workings of Tether remain remarkably opaque. New Tethers are supposed to only be minted, and added to the crypto ecosystem, when somebody gives Tether Limited dollars to create them. And if that’s how it all worked, Tether would be fine.

But there is no evidence Tether actually works this way. We repeat: There is no proof that Tether stablecoins are backed by the store of tangible assets that is supposed to justify their value.

Despite first being released eight years ago, Tether has never been audited in any way. It first promised an audit in 2017…to, you know, happen eventually. How is that coming along? As reported by the WSJ, “Tether Says Audit Is Still Months Away as Crypto Market Falters”:

Take a moment to register that: In 2017, when Tether’s total market cap was still under $1 billion, it needed a last-minute transfer of $382 million just to sly its way through a non-audit attestation of its assets. This is ominously reminiscent of the accounting trick used by borrowers to obtain so-called “liar loans” in the run-up to the 2008 subprime mortgage crash.By Jean Eaglesham and Vicky Ge Huang

Updated Aug. 27, 2022 5:33 am ET

…

Tether is designed to grease the rails of the roughly $1 trillion cryptocurrency market by promising each token can be redeemed for $1. Market observers have long questioned whether the firm’s reserves are sufficient and have been demanding audited information.

The company has been promising an audit since at least 2017. An audit is “likely months” away, said Paolo Ardoino, chief technology officer of Tether Holdings Ltd., which issues the tether coin that recently carried a market value of $68 billion.

“Things are going slower than…we would like,” Mr. Ardoino said.

Instead of a full audit, Tether, like other leading stablecoins, publishes an “attestation” showing a snapshot of its reserves and liabilities, signed off by its accounting firm.

Audits are typically more thorough than other types of attestation. The attestations for some crypto companies sign off on the numbers provided by the company’s management for a specific date and time without testing the transactions before or after that date. That process can make the reports more vulnerable to being used to paint an unduly rosy picture.

A 2017 attestation of Tether was skewed by its sister company, Bitfinex, transferring $382 million to its bank account, hours before the accountants checked the numbers, the Commodity Futures Trading Commission said last year.

[WSJ]

That 2017 attestation, incidentally, led the Commodity Futures Trading Commission to fine Tether $41 million last year, without the company admitting any wrongdoing. Tether also paid an $18.5 million fine to New York state to settle claims that it misrepresented its reserves. The settlement forced Tether and its associated Bitfinex exchange to cease operations in New York. Crucially, though, none of these fines have fully exposed how Tether works, forced it to change its methods, or even compelled it to admit wrongdoing. Tether essentially made a political payoff, it seems, and moved on.

You know things are fishy when even legendary scammer Jordan Belfort calls you out:

It’s important to state what is happening if Tether is not actually backed by the dollars that it claims. If Tether Limited is pumping out new Tethers without actually taking in an equal amount of USD, then it is essentially a privately-run money printer.

Just manufacture new Tethers, pump them into a crypto exchange, use them to buy bitcoin, then sell the bitcoin for real U.S. dollars.

That would be, in the words of Dire Straits, “Money For Nothing”:

To avoid a Dire Straits situation, in other words, the whole system must place its faith in the unaudited pinky promise of Tether’s management team. So, what remarkable financier is behind this arrangement? What person of impeccable morals is helming Tether such that it commands so much importance in the global crypto ecosystem despite doing so little to merit confidence?

Say, anybody remember the Mighty Ducks movies?

Or how about the Sinbad movie First Kid? Anybody ever catch that on The Disney Channel back in the day?

Meet Brock Pierce.

In the early 90s, Pierce enjoyed a brief career as a child actor. But before even reaching legal adulthood, Pierce pivoted into a new career, which soon ended bizarrely:

Pierce managed to get out of his Interpol jam that without being charged, and his strange path through life continued.In the trailer for First Kid, the forgettable 1996 comedy about a Secret Service agent assigned to protect the president’s son, the title character, played by a teenage Brock Pierce, describes himself as “definitely the most powerful kid in the universe.” Now, the former child star is running to be the most powerful man in the world, as an Independent candidate for President of the United States.

Before First Kid, the Minnesota-born actor secured roles in a series of PG-rated comedies, playing a young Emilio Estevez in The Mighty Ducks, before graduating to smaller parts in movies like Problem Child 3: Junior in Love. When his screen time shrunk, Pierce retired from acting for a real executive role: co-founding the video production start-up Digital Entertainment Network (DEN) alongside businessman Marc Collins-Rector. At age 17, Pierce served as its vice president, taking in a base salary of $250,000.

DEN became “the poster child for dot-com excesses,” raising more than $60 million in seed investments and plotting a $75 million IPO. But it turned into a shorthand for something else when, in October of 1999, the three co-founders suddenly resigned. That month, a New Jersey man filed a lawsuit alleging Collins-Rector had molested him for three years beginning when he was 13 years old. The following summer, three former DEN employees filed a sexual-abuse lawsuit against Pierce, Collins-Rector, and their third co-founder, Chad Shackley. The plaintiffs later dropped their case against Pierce (he made a payment of $21,600 to one of their lawyers) and Shackley. But after a federal grand jury indicted Collins-Rector on criminal charges in 2000, the DEN founders left the country. When Interpol arrested them in 2002, they said they had confiscated “guns, machetes, and child pornography” from the trio’s beach villa in Spain.

[The Daily Beast]

“Wait, is there somehow an Epstein connection here?” you might be wondering. Oh, you bet there is an Epstein connection here.

So, we have world’s third largest crypto currency, a stablecoin that has never been audited, founded by a washed up former child actor involved in a sex scandal with underaged minors that quietly dissipated without charges, who has prospered in crypto despite zero technical background, and who maintained a hard-to-explain connection to Jeffrey Epstein. But hey, Pierce says he hasn’t actually been involved with Tether since 2015. And maybe Pierce was just the “celebrity” face of the venture, and the other leaders have more legitimate background.In early 2011, about a decade after the Digital Entertainment Network imploded, [Brock] Pierce visited the Virgin Islands to attend “Mindshift,” a conference of top scientists hosted by Epstein. A representative for Pierce says he didn’t even know who Epstein was when he flew (commercial) to the event, which the financier had arranged as part of his elaborate effort to launder his lurid reputation. It was not even 18 months after Epstein had completed his slap-on-the-wrist solicitation sentence in Florida and registered as a sex offender.

…

Nothing suggests that anything of a sexual nature or anything untoward at all occurred at Mindshift. Pierce is only one of dozens of figures in Epstein’s dizzyingly vast network, and the link between the two may be nothing but a curiosity. But it is a strange tale: how a former child actor who never went to college ended up as an Epstein guest — a seemingly unlikely addition to a group that included a NASA computer engineer, an MIT professor of electrical engineering and a Nobel laureate in theoretical physics. “I don’t know what he had to do with science [or] why he was there,” says one person who attended.

[Hollywood Reporter]

Tether’s CEO is Jean-Louis van der Velde:

Hmmm… oddly sparse. Well, how about Tether’s CFO, Giancarlo Devasini?The chief executive of Tether ran a company that faced a string of lawsuits in China over unpaid bills and fines for late tax payments before he helped launch the contentious stablecoin now at the heart of the crypto industry.

As crypto has moved from finance’s fringes to its mainstream, investors have increasingly relied on stablecoins, digital tokens backed by real-world assets, as a means to buy and sell volatile currencies such as bitcoin.

But as Tether’s role in the crypto universe has mushroomed since it was founded in 2014, with $78bn of its stablecoins now in circulation, so has scrutiny from regulators. The company’s rapid rise has also turned the spotlight on publicity-shy chief executive Jean-Louis van der Velde.

The 58-year-old Dutch native’s career, spanning IT sales in Hong Kong, Germany’s software industry and an ailing Chinese electronics manufacturer, gave few hints of the significant role he would later assume.

…

While US politicians race to gather more information on Tether, even some of the group’s biggest customers say they have had few dealings with its chief executive.

Sam Bankman-Fried, the chief executive of FTX, the Hong Kong-based cryptocurrency exchange recently valued at $25bn, told the Financial Times earlier this year that he had only met van der Velde once in person.

“My sense is that he’s less involved in the external operations aspect of the business and more involved in internal management and leadership,” Bankman-Fried said. Another cryptocurrency executive who has had dealings with Tether’s management put it more bluntly: “I don’t know a lot about JL and most people don’t.”

[Financial Times]

As it turns out, “seemed like a scam” may be a fitting description of Devasini’s entire life.When Giancarlo Devasini first got into cryptocurrencies in 2012, his interests were distinctly small-time. He piped up on a popular Bitcoin forum to ask if anyone wanted to buy DVDs or CDs for 0.01 bitcoin each, then roughly 11 cents, promising free shipping for bulk orders.

Today, the 57-year-old is one of the most influential players in the global cryptocurrency marketplace. From his position as chief financial officer at Bitfinex, a major exchange, and at Tether, its sister currency which has tokens worth $60bn in circulation, industry executives say he is the key decision maker at two companies that now sit at the heart of the opaque daily flows of crypto money worth billions of dollars.

…

His first calling was as a plastic surgeon, although he quit the profession just two years out of university in 1992 after despairing at the job.

“All my work seemed like a scam, the exploitation of a whim,” he told an Italian art gallery in 2014. He recounted his particular frustration that one woman could not be talked out of reducing her breasts even though they “fit her perfectly”, as he put it.

What an incredibly sketchy character! Is anybody willing to speak up in his defense?The young doctor turned away from moulding flesh and embarked on a career dealing in electronics. He built a group of companies in Italy that, according to his Bitfinex profile page, and reiterated by Tether in response to questions from the FT, he grew to over €100m in revenue and which he says he sold shortly before the 2008 financial crisis.

Italian company documents cast his business background in a very different light. In 2007, Devasini’s business empire had revenues of just €12m and was subsequently dealt a deathblow by a devastating fire at Devasini’s warehouse and offices in February 2008. The parent company of the group, Solo, went into liquidation in June that year.

…

In 1996, not long after he had left medicine for business, he paid 100m lira — then around $65,000 — in a counterfeiting settlement with Microsoft. A decade later, in 2007, Toshiba sued another of his entities, Acme, for alleged infringement of its patents for DVD format specifications.

…

In March 2010, another of Devasini’s companies, a Monaco entity called Perpetual Action Group, was banned from Tradeloop, the online used-electronics marketplace. A month earlier, an American buyer had complained about $2,000 worth of memory chips they had bought from PAG. “[One] box was filled with a large block of wood,” the buyer claimed.

Tether says Devasini sold PAG in 2008 and was not involved with the company after that point, before clarifying that he began winding up the business in late 2009. Tradeloop’s forums in 2010 include messages showing Devasini dealing with the complaint, and messages from an associate saying Devasini had personally packed the boxes.

The funny thing about all of the above is that it’s all really obvious. Tether is apparently run by serial scammers. Its books aren’t open. It’s CEO and CFO refuse public interviews. The company’s unofficial spokesman is its CTO, who is just a developer.For Bitfinex and Tether’s customers, [Devasini] is ever present.

“He’s responsive 24/7, and he’s not just responsive to crises or unbelievable opportunities, he’s responsive to day-to-day operations,” says Sam Bankman-Fried, the chief executive of FTX, a Hong-Kong based cryptocurrency exchange.

…

Bankman-Fried says Devasini has “a lot of pride” in what he has built at Bitfinex and Tether. “He’s really grateful for the people that supported him. He’s certainly fairly annoyed at people he sees as . . . shitting on his businesses without real reason for it.”

[Financial Times]

If, as it turns out, Tether turns out to be the next FTX on steroids, the implications for the entire cryptocurrency project are existential. Tether is not just the third largest cryptocurrency in existence, its function as the dominant stable coin facilitating transactions means it is one of the major crutches upon which the entire crypto ecosystem stands.

For this reason, crypto experts tell Revolver that “true-believers” in crypto often turn a blind eye to the dark and damning questions surrounding Tether due to the implications this would have on the entire crypto project.

One crypto veteran we spoke to described the Tether situation in rather vivid terms.

“I have a soft spot for thinking kindly of crypto-libertarians, but they all go Ponzi Mindset when it comes to Tether,” he said. “In order to be congruent and confident in the future they need to believe Tether isn’t a burning bag of shit overlayed on top of a flaming diarrhetic volcano. Everything that in retrospect looks super shady and how-did-they-get-away-with-it-for-so-long for FTX is WNBA-tier compared to the 1994-Olympics Dream Team of Schemes that is Tether.”

That’s the defense of Tether from somebody who uses crypto: that Tether is an obvious scam, but with so much crypto speculation going on and so much short-term profit to be had, it’s better to just not think about it.

So, if Tether is so obviously shady, what might explain its stability even as the surrounding crypto ecosystem burns down? Some key fact is missing.

There is, for example, the strange coincidence of Tether being a crypto of choice for a U.S. government-backed rebels in Myanmar.

So it looks like US-backed paramilitary resistance funding is routed through Tether, causing pundits to ask: can stablecoins bankroll democracy?Myanmar’s shadow government said it would allow the use of the world’s largest stablecoin, Tether, as an official currency, potentially making it easier for it to raise funds and make payments.

The National Unity Government (NUG), which comprises pro-democracy groups and remnants of Myanmar’s civilian administration that was overthrown in a military coup earlier this year, has been seeking to raise funds for its “revolution” to topple the ruling military government.

The military government has outlawed the NUG and designated it a “terrorist” movement.

Tin Tun Naing, NUG’s minister in charge of planning, finance and investment, said in a December 11 Facebook post that the NUG would officially recognise USD Tether, which he said would enable better and faster transactions.

[Al Jazeera]

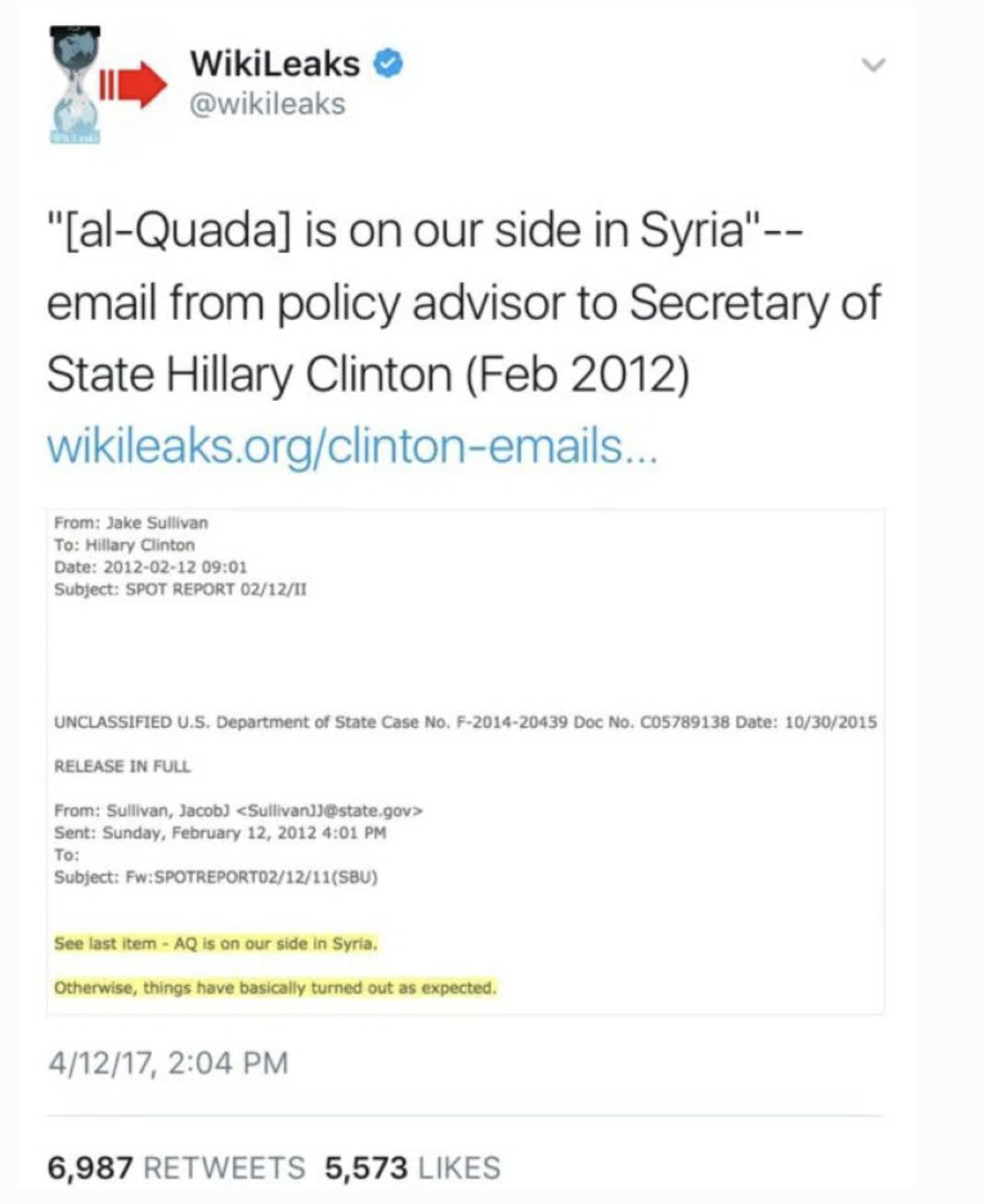

Pretty wild, huh? The al-Qaeda affiliated Sunni rebel groups of Syria also just so happen to love Tether.

The US Government’s history of backing of al-qaeda linked Sunni rebel groups in Syria has always been vexing and complicated. Remember the infamous Wikileaks-released email in which Hillary Clinton acknowledged Al-Qaeda is on our side in Syria? If only there were a mechanism to quietly launder money to these US backed groups with deniability!… BitcoinTransfer is also at the heart of a network providing money to terror groups. In August 2020, the US Department of Justice revealed BitcoinTransfer had acted as a central hub in six terror-funding operations and called for the forfeiture of 155 cryptocurrency addresses linked to the exchange. Other research has also pointed to BitcoinTransfer’s jihadist connections.

…

BitcoinTransfer itself has processed 36 bitcoin – just over $2 million based on current prices – in 679 transfers since December 2018, according to Chainalysis, a blockchain analytics firm that assisted the US indictment reported last year. Maddie Kennedy, a spokesperson for Chainalysis, says the company has not detected any further funds being sent to addresses associated with BitcoinTransfer since the August indictment. But, in the same period, BitcoinTransfer has ramped up its operations and opened new branches in Idlib while also moving from bitcoin to a stablecoin called USD-Tether. Tether is a cryptocurrency pegged to the price of the US dollar and has the highest volume of any cryptocurrency in circulation.

BitcoinTransfer opened its first store in December 2018. As well as buying and selling cryptocurrency, it runs workshops teaching people how to trade. It opened its second branch in Sarmada, a town in the north of Idlib governorate, in October 2020.

…

[A] jihadi [Telegram] trading channel shared content about a range of cryptocurrencies, including Avalanche, Cardano, Fantom, Litecoin and 1INCH, among others. A message sent to the group on March 11 appeared to be soliciting donations to supply Muslim refugees with cryptocurrency wallets and Tether. It linked a Tether address associated with the Tron blockchain. Soliciting charity is a common pattern in jihadi fundraising campaigns. In many cases, crowdfunding campaigns were military operations posing as charities – phenomena referenced in the Department of Justice indictment and that has been widely documented throughout the civil war.

[Wired UK]

Tether is not just the cryptocurrency of choice for US-backed rebel groups. It has also become a favorite of drug cartels, which, according to some journalists, are deeply intertwined with U.S. three-letter agencies, including the CIA.

Darren J. Beattie

@DarrenJBeattie

@DarrenJBeattie"Is the CIA working with the Cartels?"

5:41 PM ∙ Oct 12, 2022